It's the 15th of the month. Your accounts team has paid 200 creators. Forty of them haven't sent an invoice. Twelve sent one with the wrong VAT number. Three sent a screenshot of a Word document. One sent a voice note explaining their accountant is on holiday.

If any of this sounds familiar, the EU has a regulation that solves most of it. It's called self-billing, it's been on the books since 2010, and most finance teams either don't know it exists or don't realise it applies to them.

This article explains what a self-billing invoice is, when you can use it, how it works under EU rules, and how much time it can realistically save, with a soft landing into how modern payout software handles it automatically.

What Is a Self-Billing Invoice?

A self-billing invoice is an invoice that the buyer issues on behalf of the supplier, instead of the supplier issuing it themselves.

In a typical transaction, the seller writes the invoice and sends it to the buyer. In a self-billing arrangement, the buyer writes the invoice on the seller's behalf, sends a copy back, and treats it as if the seller had issued it. The seller (the creator, the freelancer, the artist) doesn't have to draft, format, or send anything.

It sounds backward at first. It exists because in a lot of modern business models, marketplaces, creator agencies, royalty distribution, affiliate programs, the buyer has more accurate data than the seller does about what's owed. The agency knows exactly how many videos a creator delivered. The label knows exactly how many streams happened. The platform knows exactly how many sales an affiliate drove. Asking the seller to invoice you for figures only you can compute creates an information loop that adds days of delay, errors, and back-and-forth for no benefit.

Self-billing collapses the loop. The buyer issues the invoice based on the data they already have. The seller agrees in advance that this is how the relationship works. Everyone saves time.

How It's Different From a Regular Invoice

| Regular invoice | Self-billing invoice | |

|---|---|---|

| Who issues it | Supplier (creator) | Buyer (you) |

| Source of data | Supplier computes the amount | Buyer computes the amount |

| Workflow | Supplier sends → buyer receives → buyer pays | Buyer pays → buyer generates invoice → supplier gets a copy |

| Time to payment | Days to weeks (waiting on invoice) | Immediate (no waiting) |

| Risk of errors | High (supplier may use wrong VAT, wrong details, wrong amount) | Low (buyer uses canonical data) |

| Required marking | Standard invoice fields | Must contain the words "Self-billing" or "Self-billed invoice" |

| Required agreement | None | Prior written agreement between both parties |

The critical inversion is in row two: in a regular invoice, the supplier is the source of truth. In a self-billing arrangement, the buyer is. That single change is what unlocks the time savings, and it's only legally clean if the formal requirements (the marking, the agreement) are in place.

Why Self-Billing Exists

The EU formally permitted self-billing under Council Directive 2006/112/EC, the VAT Directive, which was significantly simplified by Directive 2010/45/EU. The intent was to enable e-invoicing and automated business workflows across member states without requiring traditional supplier-issued invoices.

Different member states implemented the same framework under their own names. You'll see it called:

- Gutschriftverfahren in Germany and Austria

- Autofacturation in France

- Autofacturación in Spain

- Autofatturazione in Italy

- Self-billing in Ireland and English-language EU contexts

All of these describe the same underlying mechanism: the buyer issues the invoice, and it counts as a valid VAT invoice for both parties' books.

Outside the EU:

- The UK retained self-billing rules after Brexit under HMRC's framework. Mechanism is nearly identical.

- Switzerland permits self-billing under its own VAT law.

- The US doesn't have an exact equivalent, but uses 1099-MISC and 1099-NEC reporting forms to fulfill a similar function for payments to contractors.

For any business paying creators, freelancers, or contractors at scale across the EU, self-billing is the cleanest legally-supported way to streamline the invoicing side of the workflow.

When Can You Actually Use It? (The Three Conditions)

Under the EU framework, three things must be true for a self-billing invoice to be valid:

1. There must be a prior agreement

Before the first self-billed invoice is issued, the buyer and supplier must agree in writing that this is how invoicing will work. The agreement can be a clause inside a broader contract, it doesn't need to be a standalone document. But it has to exist, and it has to be on file.

2. The supplier must accept each invoice

There must be a procedure by which the supplier accepts each self-billed invoice. "Accept" can be implicit, e.g., not objecting within a defined period after receiving the invoice copy. The procedure needs to be agreed in advance and documented.

3. The invoice must be marked "Self-billing"

The invoice itself must explicitly state "Self-billing" or an equivalent term in the relevant language. This is a hard requirement, not a stylistic suggestion. Missing this marker can invalidate the invoice for VAT purposes.

All other standard VAT invoice fields (issue date, sequential invoice number, parties' details, VAT numbers where applicable, supply description, amounts, VAT rate or reverse charge marking) still apply.

Note: specific implementation can vary slightly by member state. Talk to your tax advisor if you have questions about how the rules apply to your particular setup.

Who Actually Benefits (Both Sides)

Self-billing is one of the genuinely rare regulatory mechanisms where both parties win. Here's how each side comes out ahead:

Your finance team

- No more invoice chasing. The invoice is generated automatically when the payout is approved.

- Consistent format across all suppliers. Every invoice has the same structure, VAT logic, and reference fields.

- No data-entry round-tripping. Because the buyer is the source of truth, the data doesn't have to be re-keyed from someone else's PDF.

- Audit trail by default. Every invoice is sequentially numbered and stored alongside the payment record. Audit prep becomes a one-click export.

Your creators, contractors, or artists

- They don't have to draft or send anything. Most creators dread invoicing. Self-billing removes that step entirely.

- They get paid faster. No more waiting for accounts to receive and process their invoice before payment can clear.

- They have a clean record. They receive a properly-formatted invoice copy for their own bookkeeping, with correct VAT handling and tax fields filled in.

- They look more professional to their own accountant. A stack of consistently-formatted self-billing invoices is easier to file than a mix of receipts and screenshots.

Note what's not on either list: any meaningful downside. The trade-off is genuinely minimal once the agreement is in place.

The 40-Hour Calculation

The headline number is realistic. Here's where it comes from.

Take a typical mid-sized creator agency or in-house brand team processing 200-250 creator payments a month.

Without self-billing, each payment requires:

- Requesting an invoice from the creator (often multiple reminders)

- Receiving the invoice in whatever format the creator sends

- Validating the invoice (correct VAT number, correct amount, correct currency, correct dates)

- Resolving errors back and forth with the creator

- Manually entering the invoice into your accounting system

Realistic average time per payment: 10-15 minutes, factoring in that roughly half of all invoices arrive with at least one issue that requires a follow-up.

With self-billing, each payment generates a compliant invoice automatically at the moment of approval. There's nothing to chase, nothing to validate, nothing to enter manually. Time per payment: under 30 seconds.

At 200 payments a month, time savings: 33-47 hours. At 300 payments, closer to 50-70.

The 40-hour figure is a conservative midpoint. For larger agencies or platforms processing thousands of payouts monthly, the savings scale linearly and quickly become a full-time-equivalent of finance team capacity.

Common Self-Billing Mistakes (and How to Avoid Them)

Most businesses that try to implement self-billing manually get tripped up by the same handful of operational issues. In rough order of frequency:

- No agreement on file. The most common error. Without a prior written agreement, the self-billed invoice isn't valid for VAT purposes. The agreement doesn't have to be elaborate, but it has to exist.

- Missing the "Self-billing" marker. The invoice has to explicitly say it. Putting it in the footer in small grey text technically counts but is often missed by auditors; clear placement is safer.

- Wrong VAT treatment cross-border. Self-billing across borders often triggers reverse charge rules. Misapplying these is a common audit finding.

- Issuing self-billing invoices to non-VAT-registered suppliers. The rules are different when the supplier isn't VAT-registered (most individual creators aren't). Modern tools handle this automatically; manual setups often don't.

- Inconsistent invoice numbering. Self-billed invoices must follow a sequential numbering scheme. Gaps or duplicates are a common audit issue.

- Not retaining records long enough. Each EU member state has its own retention requirement (typically 7-10 years). Self-billed invoices count and must be retained accordingly.

Each of these is solvable, but they're the reasons most in-house attempts at self-billing eventually get walked back to "just ask the creator for an invoice."

How Modern Payout Software Handles This Automatically

The operational complexity of self-billing is exactly the kind of work that benefits most from being absorbed by infrastructure rather than handled by humans.

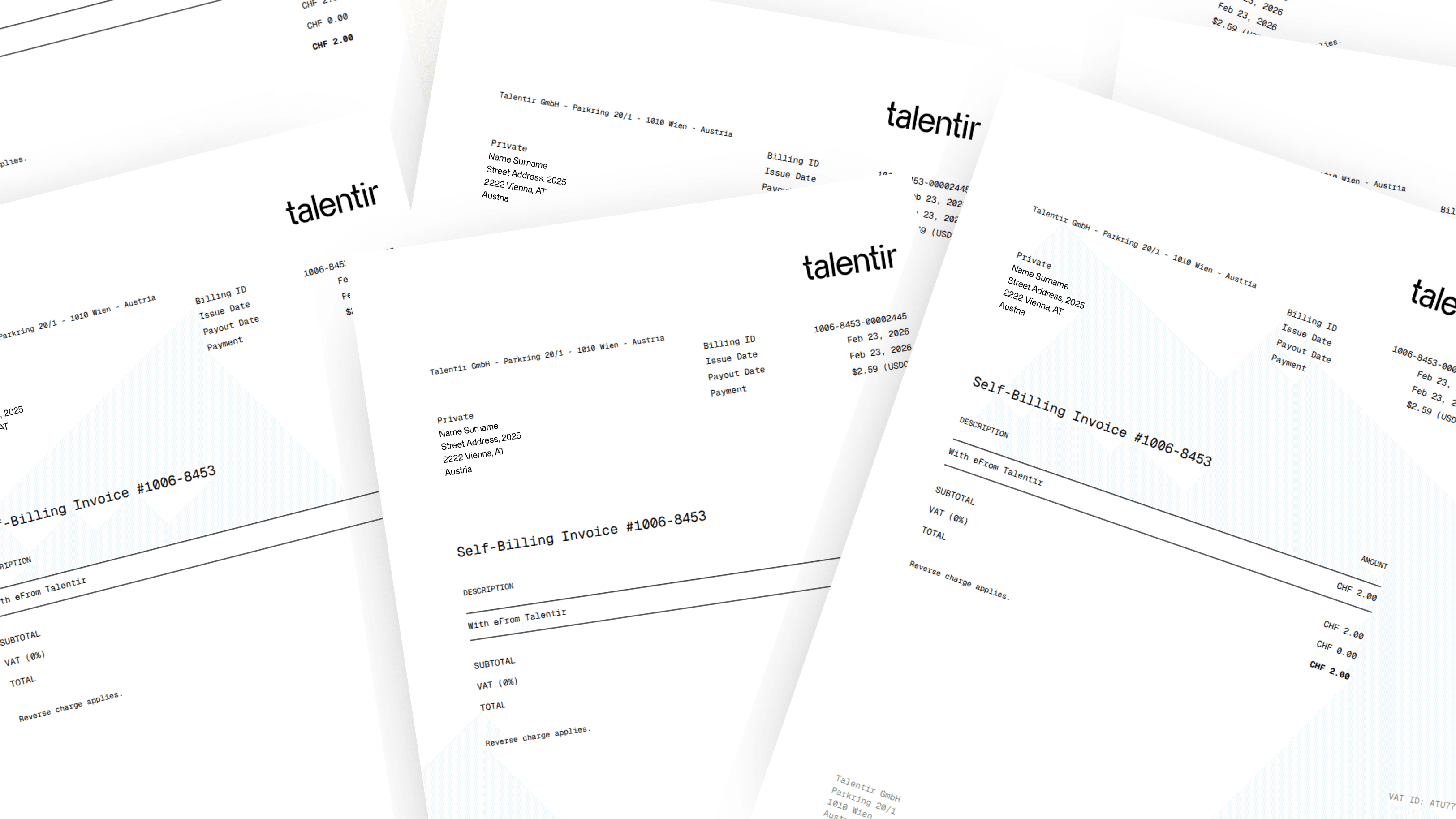

In Talentir, every approved payout generates a compliant self-billing invoice automatically:

- The invoice includes the buyer's details, the creator's details, the "Self-billing" marker, sequential numbering, and proper VAT treatment (including reverse charge where applicable)

- The supplier-agreement requirement is handled at onboarding, creators accept the self-billing arrangement when they first receive payment information

- Cross-border VAT logic is applied automatically based on the buyer's and creator's jurisdictions

- Multi-currency invoices generate in the creator's chosen currency with correct conversion documentation

- All invoices are retained, indexed, and exportable to DATEV, Odoo, or CSV in a single click

The practical effect at scale: the entire invoicing side of your creator payment workflow simply stops being a function your finance team performs.

Frequently Asked Questions

Is self-billing legal in the EU?

Yes, under the VAT Directive 2006/112/EC (amended by Directive 2010/45/EU). All EU member states recognise self-billing under their domestic implementations. The mechanism is also recognised in the UK, Switzerland, and most other developed jurisdictions in similar forms.

Do I need a written self-billing agreement?

Yes. The EU framework requires a prior agreement between buyer and supplier. The agreement can be a clause inside a broader contract and doesn't have to be a standalone document, but it has to be in writing and on file before the first self-billed invoice is issued.

Can I use self-billing for creators outside the EU?

It depends on the creator's jurisdiction and the cross-border VAT treatment that applies. In many cases yes, but with different VAT logic (often reverse charge or zero-rated). Modern payout tools handle this automatically; manual setups should consult a tax advisor.

What's the difference between self-billing and reverse charge?

They're different mechanisms that often appear together. Self-billing is about who issues the invoice. Reverse charge is about who accounts for the VAT. A cross-border self-billed invoice frequently uses reverse charge, but the two concepts are independent.

Does the creator still need to keep records?

Yes. Both parties must retain self-billed invoices for the statutory period in their respective jurisdictions (typically 7-10 years in the EU). The creator receives a copy of each invoice issued on their behalf.

What if the creator isn't VAT-registered?

Self-billing still works but with different VAT treatment, no VAT is charged, and the invoice reflects that. Most individual creators aren't VAT-registered, and any production-grade payout tool should handle this case automatically.

Can self-billing be automated end-to-end?

Yes. Modern payout software generates compliant self-billing invoices at the moment of payment approval, including the marker, sequential numbering, correct VAT treatment, and retention. This is the workflow most finance teams move toward once they understand self-billing applies to their setup.

The Short Version

If you're paying creators, freelancers, or contributors at any kind of scale in the EU, self-billing represents "the EU's officially-sanctioned answer to why am I chasing invoices from people I just paid?"

The three requirements are: prior written agreement, the "Self-billing" marker on each invoice, and a procedure for supplier acceptance. Everything else is operational logistics, which is exactly the kind of work that benefits most from being absorbed into payout infrastructure rather than handled by a finance team manually.