Most articles about stablecoin payouts open with the word "revolutionising."

This one won't.

Stablecoins are not a revolution. They are a payment rail — one that happens to be faster and cheaper than bank wires for certain cross-border use cases, and one that finance teams can use without engaging with anything that looks or feels like crypto. The version of stablecoins that's relevant to a CFO has almost nothing in common with the version that's relevant to a Twitter thread.

This article explains what stablecoins are in finance-team language, what problem they actually solve for business payouts, the genuine concerns worth taking seriously, and when (and when not) they make sense.

What Stablecoins Actually Are

A stablecoin is a digital token that's designed to maintain a fixed exchange rate against a fiat currency. The two relevant to business payouts:

- USDC — a token pegged 1:1 to the US dollar, issued by Circle (a US-regulated financial company). Each USDC in circulation is backed by US dollar reserves held with regulated custodians, attested monthly by Deloitte.

- EURC — a token pegged 1:1 to the euro, issued by Circle under the EU's MiCA regulatory framework (which came into force for stablecoins on 30 June 2024). Same model, euro-denominated.

Functionally, a USDC is a digital claim on a dollar held in reserve. A EURC is a digital claim on a euro held in reserve. They move on blockchain networks (Talentir uses Base, an Ethereum-based network operated by Coinbase) which means transfers settle in seconds and cost cents — versus the days and percentage-point fees of traditional bank rails.

That is the entire mechanism. There is no investment thesis. There is no yield play. There is no need for the reader of this article to ever buy, hold, or speculate on anything.

What Problem They Solve for Business Payouts

Bank rails were designed for a different era. Cross-border bank transfers take 2-5 days, cost €20-50 in fixed fees plus 3-5% in FX spread, and stop running on weekends and holidays. SWIFT messages get rejected for opaque reasons. Intermediary banks take silent cuts at each hop.

For a business paying a single supplier once a quarter, this is annoying but manageable. For a business paying hundreds of creators, freelancers, or contractors every month across multiple countries, it's a structural cost.

Stablecoin transfers solve four specific frictions:

- Speed. Cross-border settlement in seconds rather than days. A creator in São Paulo or Mumbai gets paid at the same moment as a creator in Berlin.

- Cost. Network fees on Base are typically under €0.10 per transfer, regardless of amount. The 3-5% FX spread on bank rails simply doesn't exist.

- Always-on. No weekends, no holidays, no banking cut-off times. A payment approved on a Sunday goes out on a Sunday.

- Predictability. What the sender intends to send is what the recipient receives. No silent intermediary-bank fees mid-route.

None of these properties require the recipient to care about crypto. They can convert the stablecoin to local fiat through their own banking provider, spend it directly via stablecoin-linked debit cards (now offered by several major payment networks), or hold it briefly until conversion. The choice belongs to the recipient. The cost saving belongs to the business.

The Concerns Worth Taking Seriously

Here are the questions a competent finance team will ask. Each one has a real answer.

“What if the stablecoin depegs?”

The most-cited example: in March 2023, USDC briefly dropped to around $0.87 when Circle disclosed that ~$

What the event proved was that reserve transparency works (Circle disclosed quickly, markets repriced accurately) and that stablecoin depegs are concentration-risk events, not architectural failures. Since 2023, Circle has materially restructured its reserve custody to avoid concentration in any single banking partner.

The honest answer for finance teams: stablecoin depeg risk is real but bounded, comparable in shape to money-market-fund "breaking the buck" risk that institutional treasurers have managed for decades. For a business that holds stablecoins only briefly as a payment rail (rather than treasury), the risk window is measured in minutes between deposit and payout — not months.

“Is this legal?”

In the EU, stablecoin issuance and circulation are now formally regulated under MiCA (Markets in Crypto-Assets Regulation), effective for stablecoins since 30 June 2024. EURC was specifically designed to comply with MiCA's stricter requirements for euro-denominated stablecoins.

In the US, USDC operates under state-level money transmission licensing held by Circle. In the UK, Switzerland, Singapore, and most other developed jurisdictions, equivalent frameworks exist or are emerging.

What this means in practice for a business using stablecoins as a payment rail: yes, it's legal in every major jurisdiction where you're likely to be paying creators. Your tax advisor should validate specifics for your jurisdiction, but the "is this legal" question is settled.

“How is this treated for accounting?”

Stablecoins are currently treated as intangible assets under most accounting standards (IFRS, US GAAP). For a business that holds stablecoins briefly as a payment rail — deposit fiat, convert to stablecoin, send to creator, all within minutes — the holding window is short enough that the accounting treatment is largely procedural.

This is an area where the rules are still evolving (FASB issued updated guidance in late 2023; IFRS guidance is in active discussion). Specifics matter for your auditor. The high-level picture: stablecoin-based business payouts are not an accounting frontier; they are a known and increasingly standard treatment.

As with the self-billing explainer, this article does not constitute formal tax or accounting advice. Consult your auditor for guidance specific to your setup.

“Who holds the money in between?”

In a properly-designed stablecoin payout flow, the answer is nobody — the funds spend essentially zero time held by any intermediary, because conversion and transfer happen near-atomically. This is structurally safer than the bank-rail equivalent, where SWIFT correspondents may hold funds for 1-3 days at each hop.

What matters operationally is the regulatory status of the on-ramp/off-ramp provider (e.g., the entity that converts your EUR into EURC and back). For Talentir, this is handled by regulated partners within the MiCA framework.

“Will my creators have to use a crypto wallet?”

No. The creator chooses how they receive payment — bank transfer in local currency, PayPal, Venmo, or stablecoin. Creators who actively want stablecoin (typically for cross-border speed, or because they hold currencies that are themselves unstable) can opt in. Creators who don't, never see it.

The stablecoin rail is invisible to the recipient unless they choose otherwise.

When Stablecoin Payouts Actually Make Sense

Stablecoin payouts are not always the right rail. The honest matrix:

Strong fit:

- Cross-border payments where speed matters (creator marketing, royalty distribution, affiliate commissions to global partners)

- High-volume, low-value payouts where bank-rail fixed fees would dominate the transaction

- Payments to creators in countries with unstable local currencies who prefer to hold USD-denominated value

- Weekend and after-hours payments where bank rails simply don't move

Weak fit:

- Domestic SEPA or ACH payments where bank rails are already fast and cheap

- Payments to recipients in highly-banked countries who specifically prefer their local bank

- Any situation where the recipient's regulatory environment makes stablecoin receipt complex (a small but real list of jurisdictions)

The right framing isn't "stablecoins replace bank transfers." It's "stablecoins are a payment rail you can offer alongside bank transfers, used by creators when they make sense and not used when they don't."

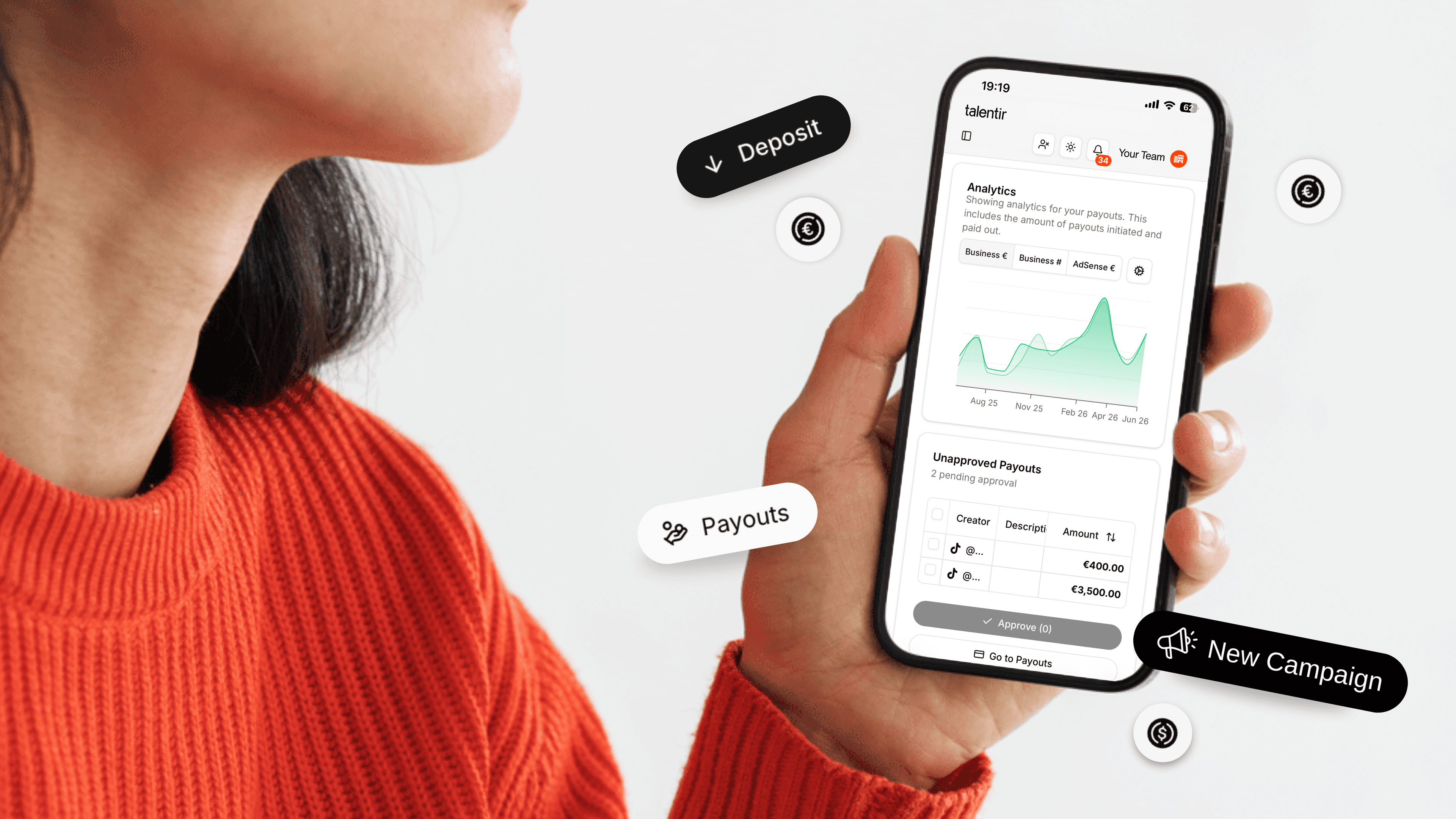

What a Stablecoin Payout Workflow Actually Looks Like

In practice, with Talentir, the workflow is:

- You fund your Talentir wallet in EUR or USD. Regular bank transfer. No crypto on your side.

- Your team creates a payout for a creator, just like any other payout.

- The creator picks how to receive it. If they choose stablecoin, USDC or EURC. If they choose bank transfer or PayPal, that's what they get.

- The payout settles in seconds for the stablecoin option, with a network fee of cents rather than a 3-5% FX spread.

- A compliant self-billing invoice generates automatically, regardless of which rail was used.

- The transaction is logged, included in your reporting, and exportable to DATEV, Odoo, or CSV with the rest of your payouts.

From your finance team's perspective, nothing about the operational flow looks different from a regular payout. Stablecoin is a rail under the hood. Above it, the experience is the same accounting export, the same invoice format, the same dashboard view.

Frequently Asked Questions

Are stablecoin payouts legal for businesses in the EU?

Yes. Under MiCA (the Markets in Crypto-Assets Regulation, effective for stablecoins from 30 June 2024), euro-denominated stablecoins like EURC are formally regulated. USD-denominated stablecoins like USDC also operate within the MiCA framework for EU usage. As always, specifics for your jurisdiction should be confirmed with your tax advisor.

What's the difference between USDC and EURC?

USDC is pegged 1:1 to the US dollar; EURC is pegged 1:1 to the euro. Both are issued by Circle and backed by fiat reserves attested monthly. Choose USDC if you or your creators primarily reference USD-denominated value; choose EURC for euro-denominated workflows. Most payout platforms support both.

Are stablecoins safe?

Stablecoins are not risk-free, but the risks are bounded and well-understood. The main risk is brief depegging during reserve stress events (see USDC's March 2023 depeg, which restored within days). For businesses using stablecoins as a transient payment rail rather than treasury holdings, the exposure window is minutes, not months.

How are stablecoin payouts taxed?

Stablecoin payouts are taxed the same as any other business payment to a contractor or creator. The recipient owes income tax on the value received in their local jurisdiction; the business deducts the payment as a normal expense. Use of a stablecoin rail does not change the underlying tax treatment.

Do my creators need a crypto wallet?

Only if they specifically choose to receive payment in stablecoin. Creators who prefer bank transfer, PayPal, or Venmo never need to engage with stablecoins at all. The recipient chooses the payment method.

Can I send in stablecoin and have my creator receive bank transfer?

With a payout platform that supports multi-rail conversion (Talentir does), yes. The platform handles the on-ramp/off-ramp conversion transparently. From your side, you see "payout sent." From the creator's side, they see a deposit in their preferred method and currency.

What if USDC depegs again?

For a business using stablecoins as a payment rail (rather than holding them as treasury), exposure to a depeg event is limited to the brief window between deposit and payout — typically minutes. The structural risk is meaningfully lower than holding stablecoins as a balance-sheet asset.

The Bottom Line

Stablecoins are a payment rail. That's the entire story for businesses that need to move money to creators, freelancers, or contributors at scale.

The technology is regulated where it matters, transparent in how it operates, and bounded in its risk profile. The use case for business payouts — cross-border speed and cost reduction, without making the recipient engage with anything they don't want to engage with — is one of the few applications where the practical benefits clearly outweigh the operational overhead.

If any of this article reads as "non-revolutionary," that's the point. Most finance teams want their payment infrastructure to be exactly that.

Sign up now or book a call — your first stablecoin payout can go out within 72 hours, and your finance team can keep their existing accounting workflow.